Action Construction Equipment Ltd. (ACE): Inside the Machinery of India’s Industrial Cycle

A deep forensic and strategic examination of how ACE’s balance-sheet discipline, product diversification, and market alignment mirror India’s multi-sector capex cycle.

1. A Quiet Engine of Industrial India

In the Indian equity landscape, certain companies sit quietly behind the skyline they help construct. Action Construction Equipment Limited (ACE) is one of them.

Over the last half-decade, ACE has transitioned from being a domestic crane manufacturer into a diversified capital-goods platform spanning cranes, construction machinery, material-handling systems, and agri-equipment, with an emerging footprint in defence engineering and exports.

Its story is about compounding through operational discipline, a philosophy that fits squarely within India’s ongoing infrastructure-driven investment cycle.

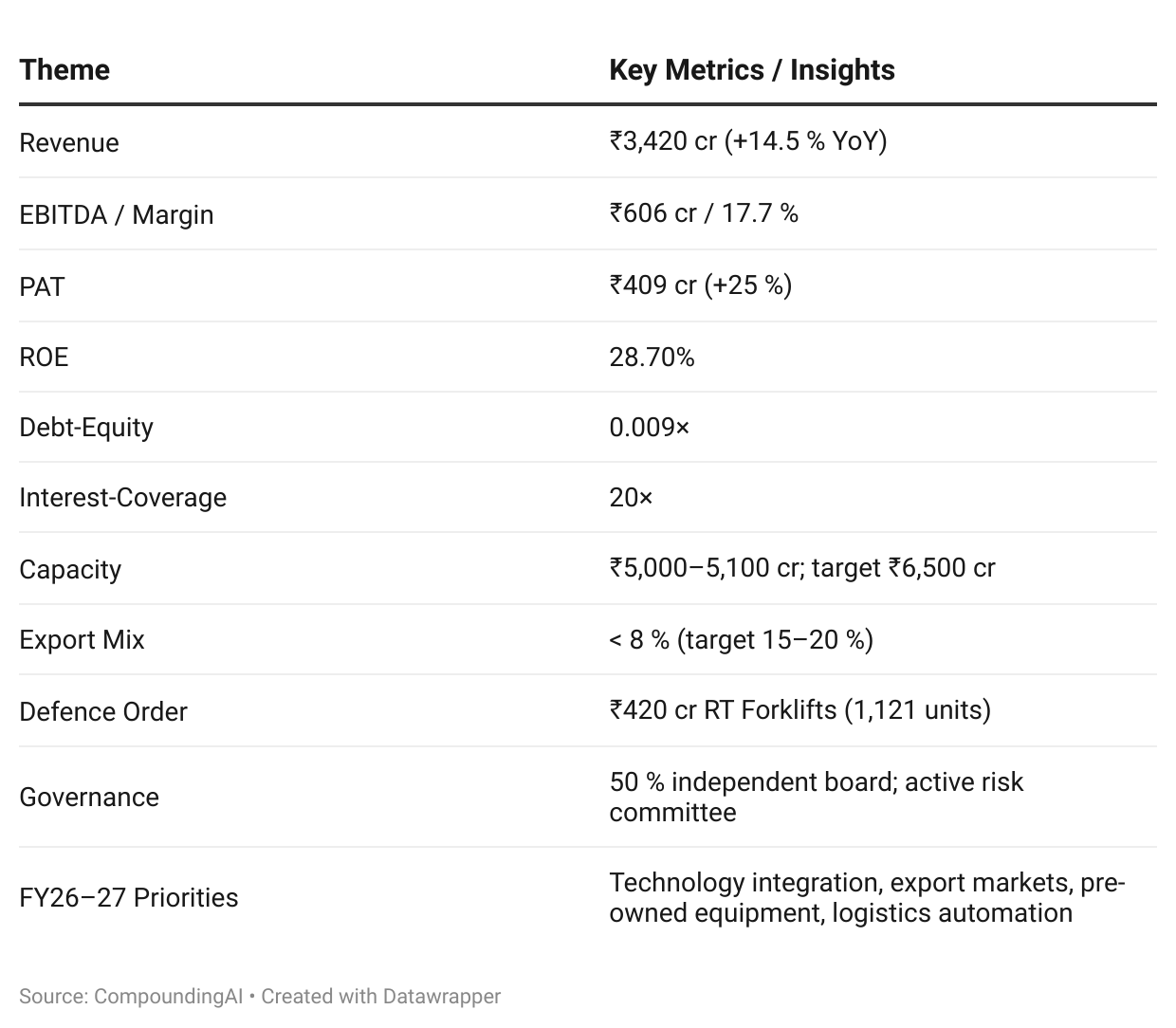

In FY25, ACE’s consolidated income reached ₹3,427 crore, up 15 % YoY. EBITDA stood at ₹606 crore (margin 17.7 %), while PAT rose 25 % to ₹409 crore. These figures are not exceptional in isolation, but they represent consistent execution across cyclical and structural shifts, achieved with minimal leverage and methodical capital allocation.

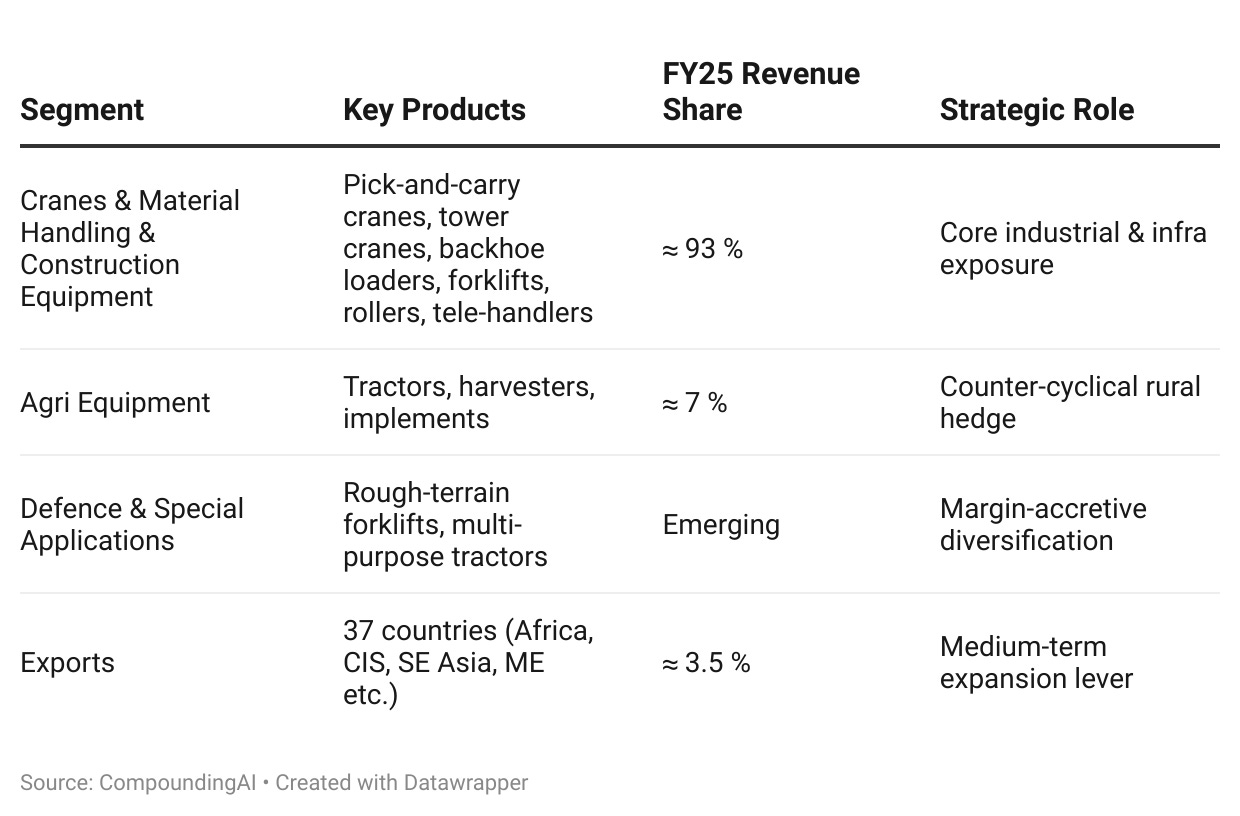

2. Business Model: Four Engines of a Diversified Enterprise

ACE’s model reflects the anatomy of India’s capital-goods ecosystem: infrastructure, manufacturing, agriculture, logistics, and now defence.

ACE is the world’s largest pick-and-carry crane manufacturer (≈ 63 % global share) and India’s leader in tower cranes (> 60 % domestic share).

It operates eight plants (six at Dudhola, Haryana), 19 regional offices, one overseas office, and an extensive dealer/service network across 28 states + 8 UTs.

Operating Geometry

Cranes remain the flagship vertical and the most cyclical.

Construction & material-handling act as industrial adjacencies.

Agri machinery balances monsoon-linked rural cycles.

Defence orders introduce stability and higher realizations.

The model’s internal hedging across business cycles exemplifies the kind of balance-sheet thinking that characterizes well-run Indian mid-caps.

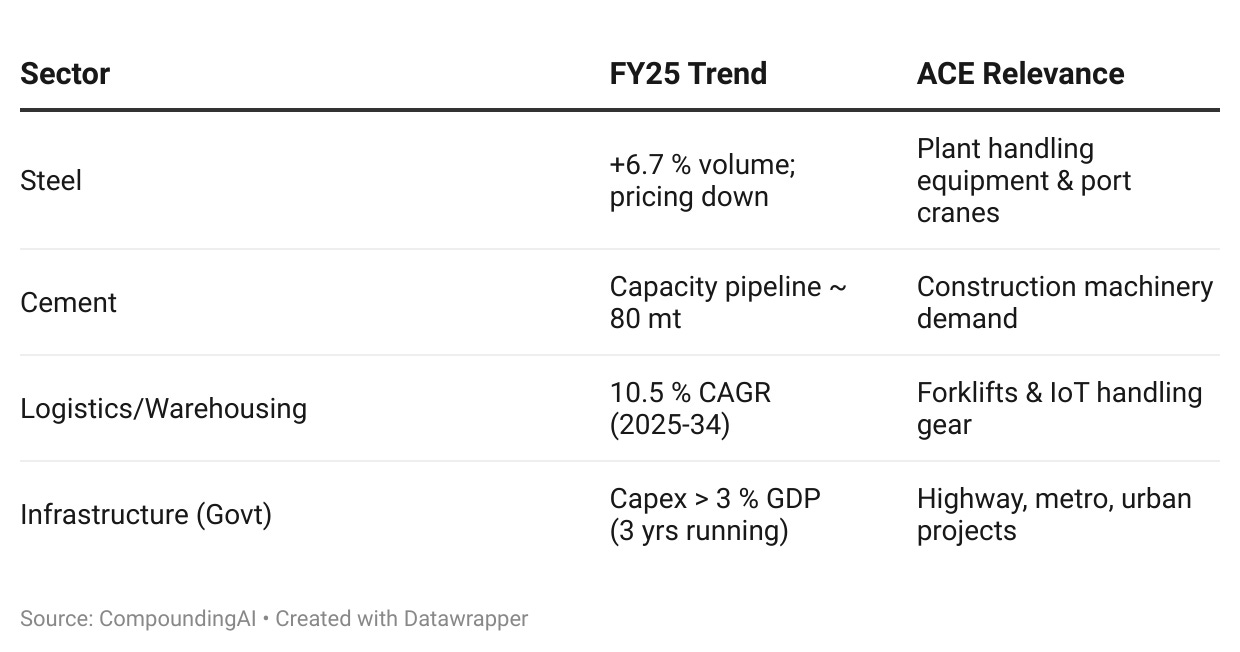

3. Sectoral Tailwinds: The Macro Bridge to ACE’s Micro

FY25 unfolded against a macro backdrop of government-led capital formation.

Infrastructure Capex: The Union Budget FY26 sustained a record ₹ 11.21 lakh crore allocation, continuing a three-year streak of public capex exceeding 3 % of GDP.

Manufacturing Resurgence: PLI schemes and “China + 1” shifts accelerated industrial spending, creating demand for plant-level cranes and logistics equipment.

Agriculture Mechanization: Rural prosperity and subsidy programs like PM Dhan-Dhaanya Krishi Yojana boosted tractor and harvester penetration.

Warehousing & E-Commerce: India’s warehousing market is projected to grow 10.5 % CAGR (2025-34) to USD 163.9 billion, a direct multiplier for forklifts and material-handling systems.

ACE’s diversified exposure lets it monetize all these vectors simultaneously.

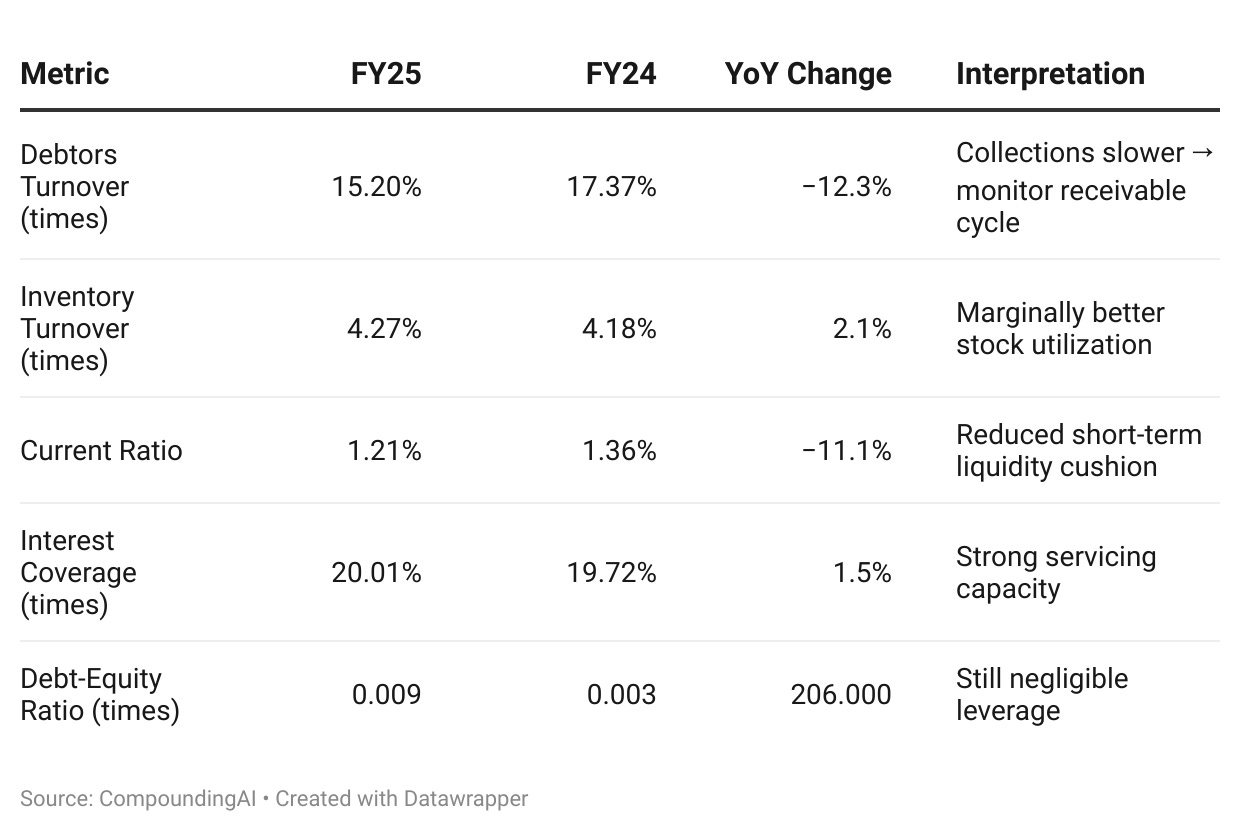

4. Financial Discipline: Working Capital and Leverage

ACE’s FY25 ratios reveal tight fiscal control amid expansion.

Interpretation

ACE remains effectively debt-free in structural terms. The minor rise in borrowings from ₹ 4.2 crore to ₹ 14.7 crore, stems from capacity expansion, not stress.

Interest coverage above 20× underscores surplus operating cash.

The modest decline in current ratio and debtor efficiency signals working-capital absorption, typical during build-out phases. Overall, balance-sheet discipline remains strong.

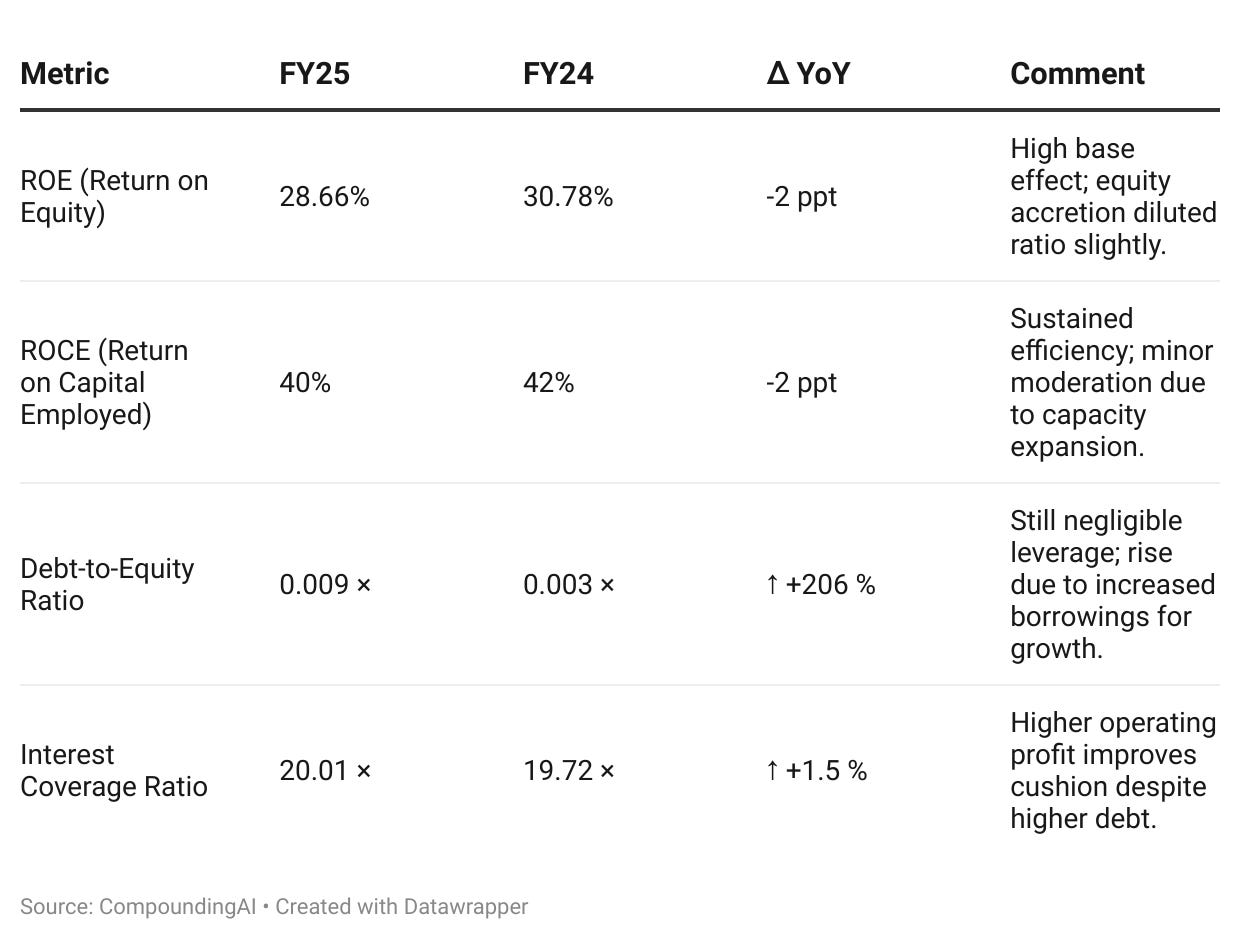

5. Returns and Capital Deployment

Interpretation

ACE continues to exhibit best-in-class return ratios for a mid-cap engineering firm.

A slight decline in both ROE and ROCE stems from fresh capacity build-out and an enlarged capital base, not deteriorating profitability.

With ROCE consistently above 40 %, the company remains among the most efficient capital allocators in India’s construction-equipment space, a level comparable to or higher than most peers in the capital-goods sector.

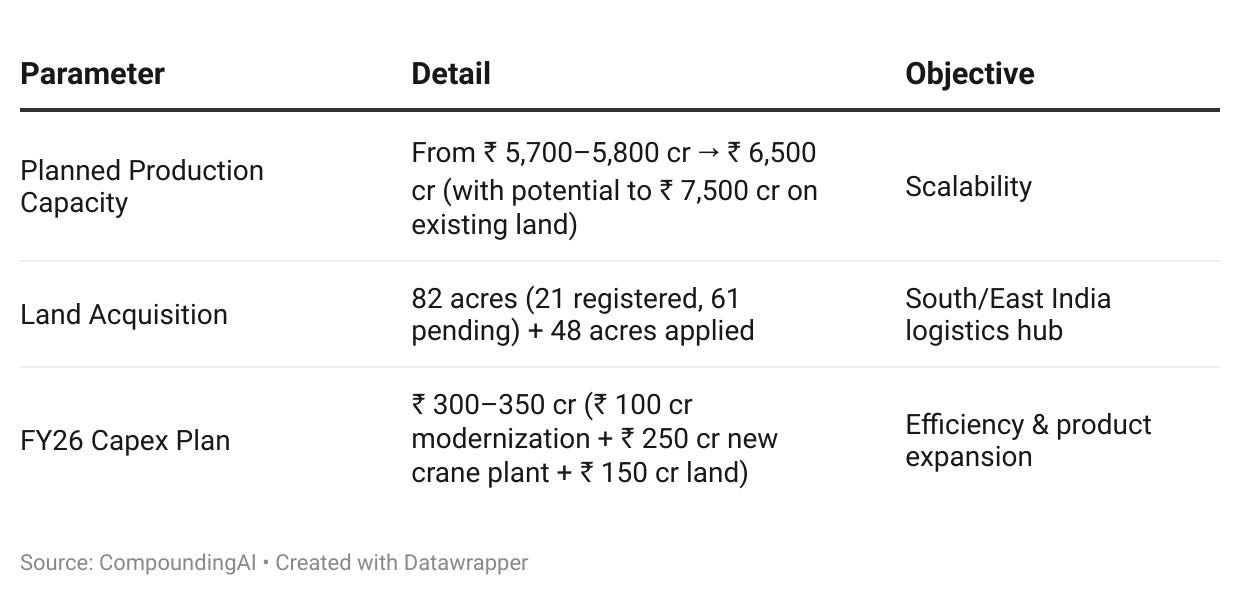

6. Capacity Build-out: Preparing for the Next Upcycle

By Q4 FY25, ACE’s revenue-handling capacity had reached ₹ 5,000–5,100 crore, aligning with its medium-term target to double FY23 levels.

Order Visibility

FY25 total income ₹ 3,420 cr (+14.5 %).

Cranes & Material Handling segment ₹ 3,090 cr (+15.5 %).

Defence Order: 1,121 RT Forklifts worth ₹ 420 cr , ACE’s largest ever, execution from FY26.

Manufacturing + Logistics Exposure: ≈ 45 % of revenue; Infrastructure ≈ 35 %.

These indicators link ACE directly to India’s industrial-capex corridors.

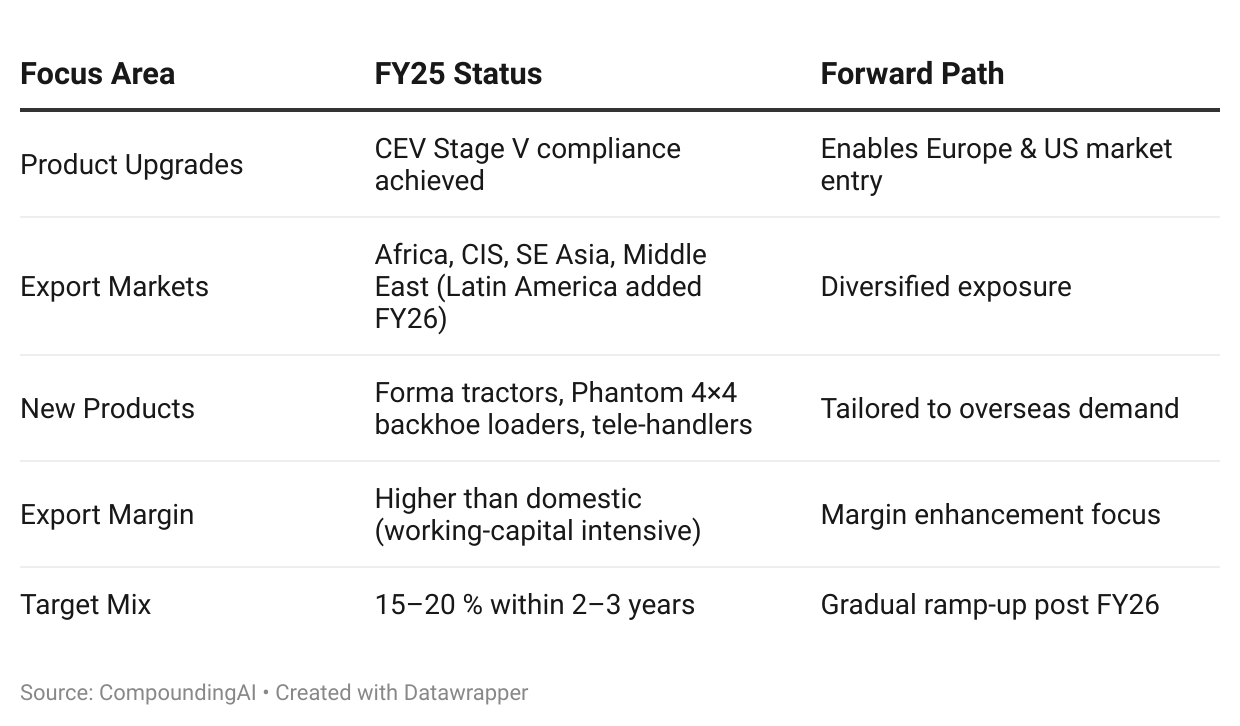

7. Export Strategy: Setting the Stage Beyond India

Exports contributed < 8 % of FY25 revenue (≈ ₹ 270 cr).

Short-term headwinds - high freight, geopolitics, tariffs, kept numbers below the 15–20 % target.

Yet the framework for expansion is in place.

Combined defence + export share is expected to touch ≈ 10 % of revenue by FY27, a meaningful de-risking from purely domestic cycles.

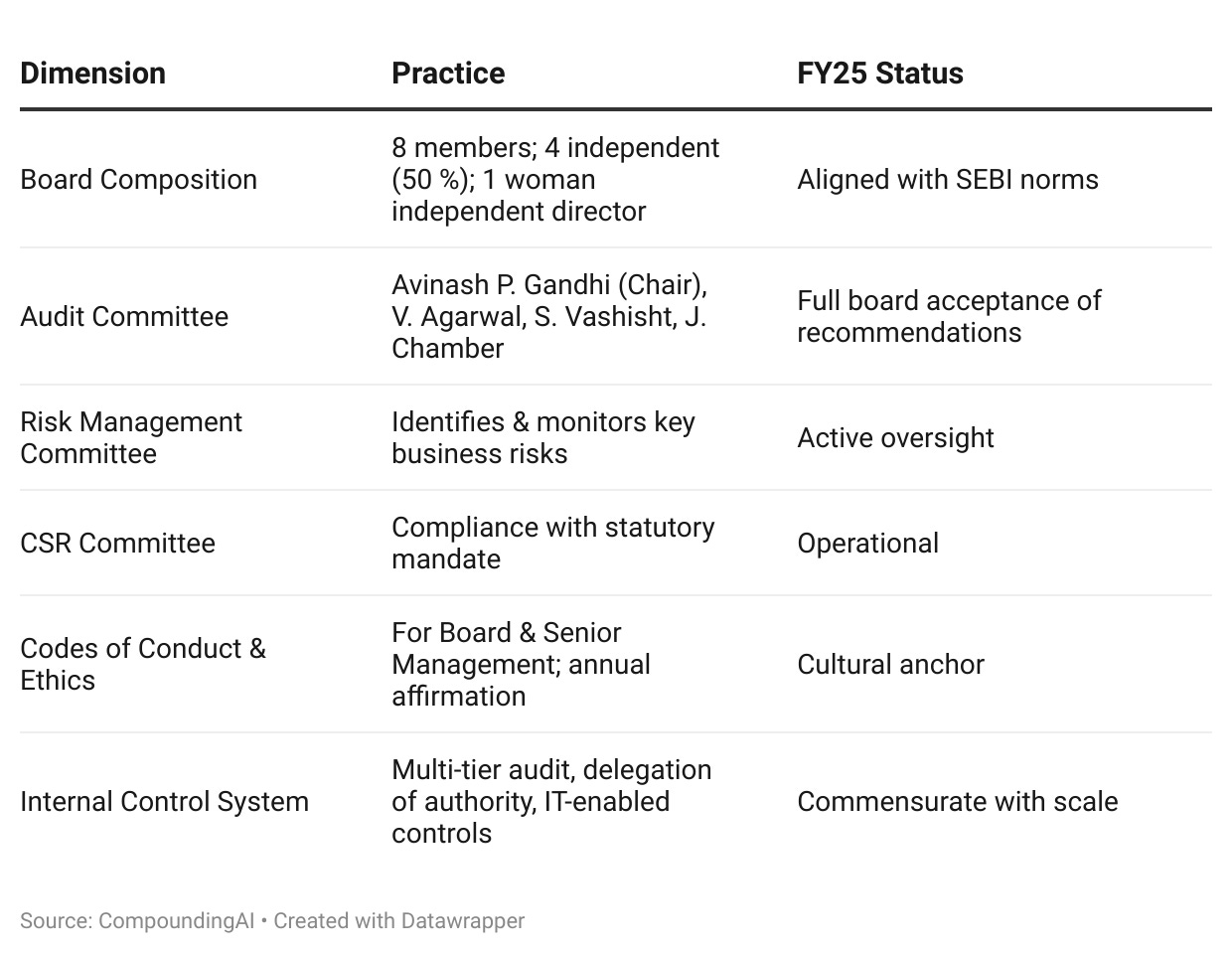

8. Governance, Oversight, and Risk Management

ACE’s disclosures demonstrate an institutional governance posture uncommon in many mid-caps.

Risk Framework

The enterprise-risk matrix covers eight clusters - economic, market, operational, raw material, regulatory, demand, financing, and reporting.

Each is overseen by the Risk Management Committee and validated by internal audit.

This institutional layering enables foresight rather than reactive management, a key differentiator for investors assessing governance quality.

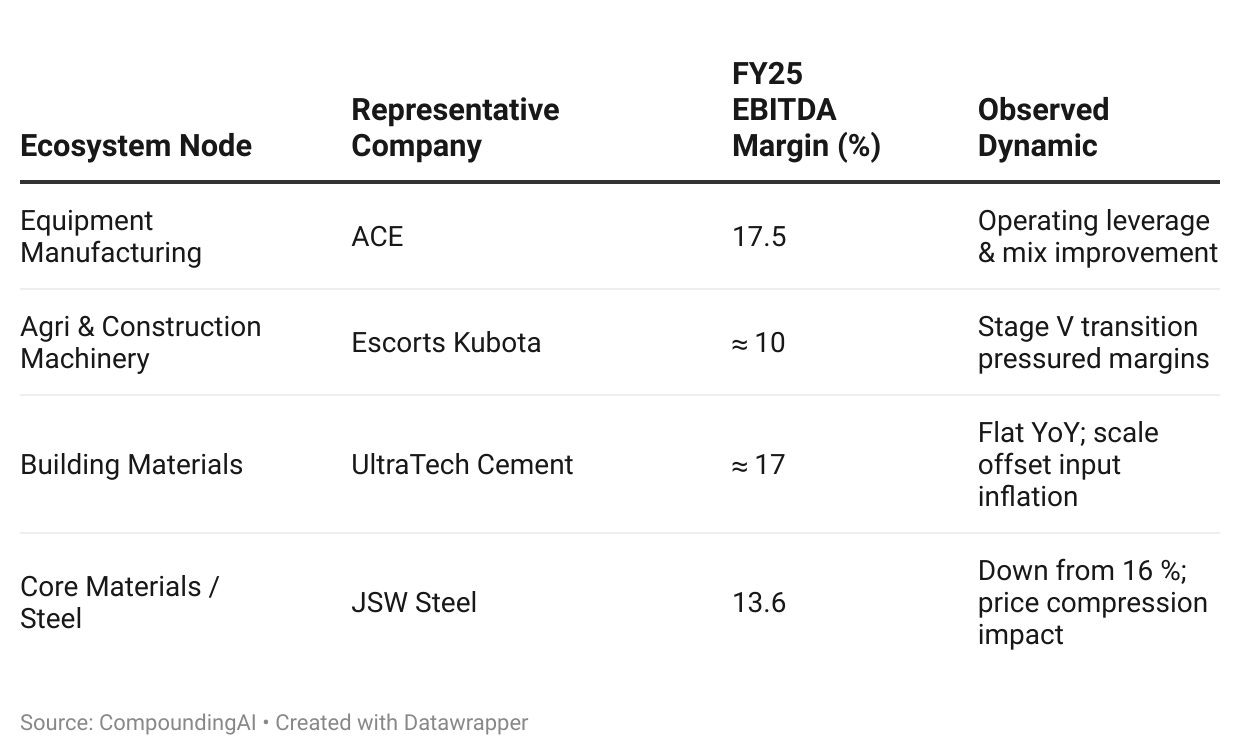

9. ACE in the Capital-Goods Ecosystem: Indirect Comparisons

Instead of head-to-head peers, ACE aligns with adjacencies that mirror the capital-investment chain.

Interpretation:

ACE’s margin profile now parallels large-cap materials companies despite its smaller scale, highlighting structural profitability from process discipline rather than commodity leverage.

Its cyclical exposure is closer to construction materials but with higher capital turns and less raw-material volatility.

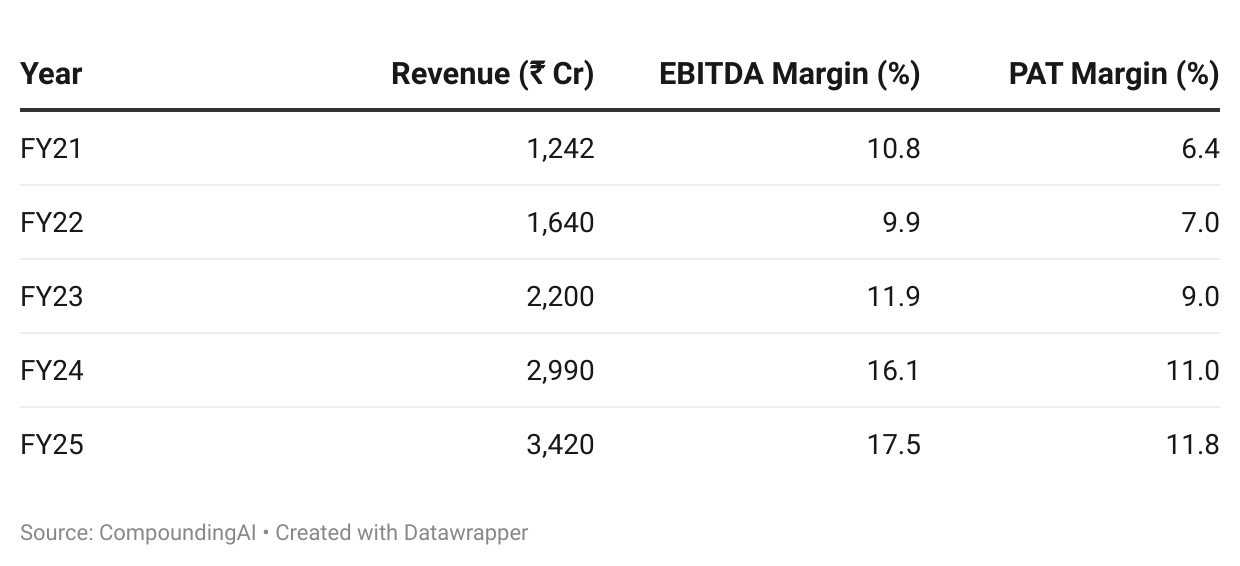

10. Multi-Year Revenue & Margin Arc (FY21 - FY25)

Five-Year CAGR

Revenue +28 %

EBITDA +41 %

PAT +43 %

Comparative Narrative

Cement (Shree, UltraTech): 5–7 % CAGR; margin volatility with energy costs.

Steel (JSW): Topline flat; margin -250 bps YoY.

CV OEMs: Volume rebound but thin price spread.

ACE stands out for steady upward trajectory rather than oscillating cycles.

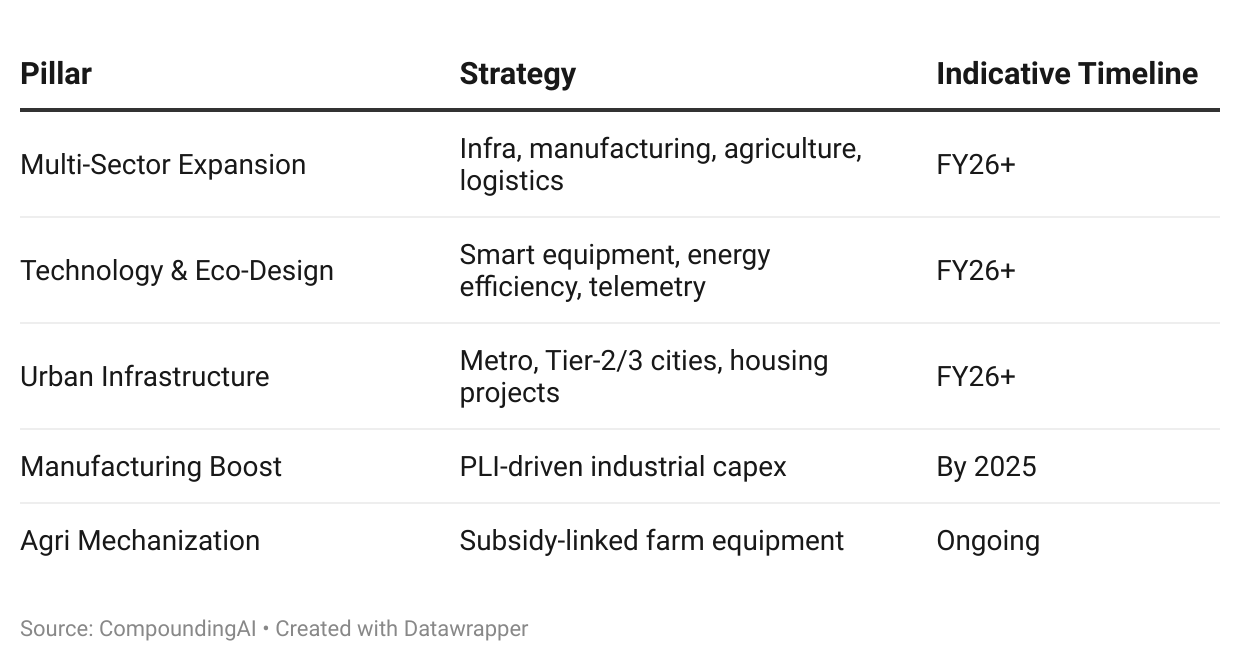

11. Strategic Priorities FY26 - FY27

ACE’s management roadmap integrates growth, technology, and sustainability.

Management commentary links these themes to long-term competitiveness rather than short-term revenue targets.

12. Alignment with India’s Industrial-Capex Wave

ACE’s revenue distribution : 45 % manufacturing/logistics, 35 % infrastructure, makes it a near-proxy for India’s fixed-capital-formation index.

13. Operational Headwinds

Even disciplined operators face constraints:

Seasonality & Election Pause: H1 FY25 saw muted execution; rebound H2.

Export Logistics: High freight & tariffs curbed volumes.

Rural Demand: Erratic monsoon hit tractor offtake.

Competitive Pressure: Low-cost imports in large-crane segment.

Skill Availability: Advanced equipment operation training gap.

Mitigation plans include automation, training institutes, and domestic supplier integration to de-risk imports.

14. Management Communication & Governance Tone

Investor interactions emphasize clarity over guidance:

Consistent quantification of drivers (working capital, mix, cost structure).

Conservative commentary, rarely over-promising.

Transparent acknowledgment of seasonal volatility, export delays, and demand swings without narrative gloss.

This tone of data-first conservatism aligns with how investors prefer management communication: factual, tempered, and verifiable.

15. Broader Analytical Reflection

ACE represents a clean case study in how India’s public-capex multiplier diffuses through downstream industries.

Government spending in steel, cement, and logistics transforms into orders for cranes, forklifts, and agri-machinery, the products ACE builds.

Its trajectory therefore mirrors the rhythm of the broader economy rather than any single sector.

Yet neutrality requires acknowledging limits:

Export ambitions, though credible, remain aspirational until sustained double-digit contribution materializes.

Working-capital intensity is structurally high due to receivables from EPC and public clients.

Agri-equipment remains sub-10 % of turnover, limiting true counter-cyclicality.

Execution scalability beyond ₹6,500 crore capacity will test operational controls.

Still, compared with most mid-cap manufacturers, ACE’s governance transparency, financial prudence, and steady capital efficiency present a low-volatility compounding profile.

16. Neutral Outlook

ACE enters FY26 with balanced momentum:

Capacity ready: ₹5,000-plus crore revenue capability with further room.

Order visibility: Defence, infra, and industrial manufacturing pipelines healthy.

Balance-sheet strength: Debt negligible; cash flows positive.

Macro tailwinds: Capex cycle intact through FY27 budgets.

Risks remain from export cyclicality and monsoon-linked agri softness, but structural direction stays positive.

In summary, ACE is a measured industrial compounder, mirroring India’s broader investment story in microcosm.

Summary Table: FY25 Snapshot

17. Final Perspective

For portfolio managers seeking exposure to India’s industrial-capex cycle without raw-material volatility, ACE sits in the middle of the value chain between upstream metals and downstream infrastructure execution.

It converts national expenditure into tangible machinery, bridging fiscal policy and field-level productivity.

Its evolution from a crane maker to a diversified capital-goods integrator underscores three traits that define India’s manufacturing resurgence:

Operational sobriety – tight working-capital discipline.

Incremental innovation – technology upgrades over speculative bets.

Governance credibility – structured oversight uncommon among peers.

ACE may not deliver explosive quarterly surprises, but for investors and analysts evaluating long-duration industrial exposure, it remains a steady mirror to India’s build-out decade.

Note : Not a buy/sell recommendation. For education purpose only.

This piece is created using inputs only from CompoundingAI.

CompoundingAI is an enterprise-grade vertical intelligence engine that transforms unstructured corporate filings into decision-grade insights within minutes, complete with source-level traceability for confident, auditable workflows.

We cut the noise & directly deliver insights.